CBM Bancorp (CBMB) Buyout

Rosedale Federal Savings & Loan Association to acquire CBM Bancorp for $64.4 million

Greetings and happy Saturday! My goals for Conversion Confidential are essentially threefold: 1) to educate others (and learn more myself) about banks and thrift conversions, 2) to provide investment research and analysis on this niche space, and 3) to cover general news relevant to thrift conversions, with the caveat I will not be a comprehensive source for all activity.

This week’s Conversion Confidential falls into bucket number three as there’s some thrift conversion merger and acquisition (M&A) news to highlight! I do not own shares in CBMB and have not done a deep-dive on them so I’ll try to be brief. If you’re looking for more, last week’s profile of NSTS Bancorp was a bit more in depth for those of you who haven’t read it yet.

On Friday, Rosedale Federal Savings & Loan Association, another local Baltimore bank agreed to acquire CBMB for $64.4 million, or $17.75 in cash per share. CBMB was originally a standard conversion back in September of 2018 so this outcome came about as quick as they can (recall there is a three year moratorium on mergers when a thrift converts to public ownership). The merger is expected to close in 1H22 and the full release can be read here.

CBMB shares, which had closed Thursday afternoon at $14.10 quickly jumped 21% to $17.10 on the news. Assuming an investor bought near $12.50 / share (~88% of then TBV and about where it traded the first few months post-conversion) and holds until the end of the expected 1H22 closing, they would’ve obtained an approximate 12% IRR, including dividends. Not world-beating, but not too shabby either! By averaging down opportunistically or by participating in the original subscription offering, an investor would’ve obviously achieved even higher returns.

So what can we learn from this event? According to the 4Q21 FDIC call report, which also posted on Friday, CBMB was well capitalized, marginally profitable, and bought out at a premium to tangible equity. Hopefully, you’re noticing somewhat of a pattern to the things I look for in thrifts. Here are a couple quick stats:

4Q21 equity to assets ratio of 18.7%

2021 return on assets (ROA) of 0.60%

Non-interest bearing deposits to total deposits of 19.5%

Takeout price implies nearly 1.4x TBV and a ~13% core deposit premium

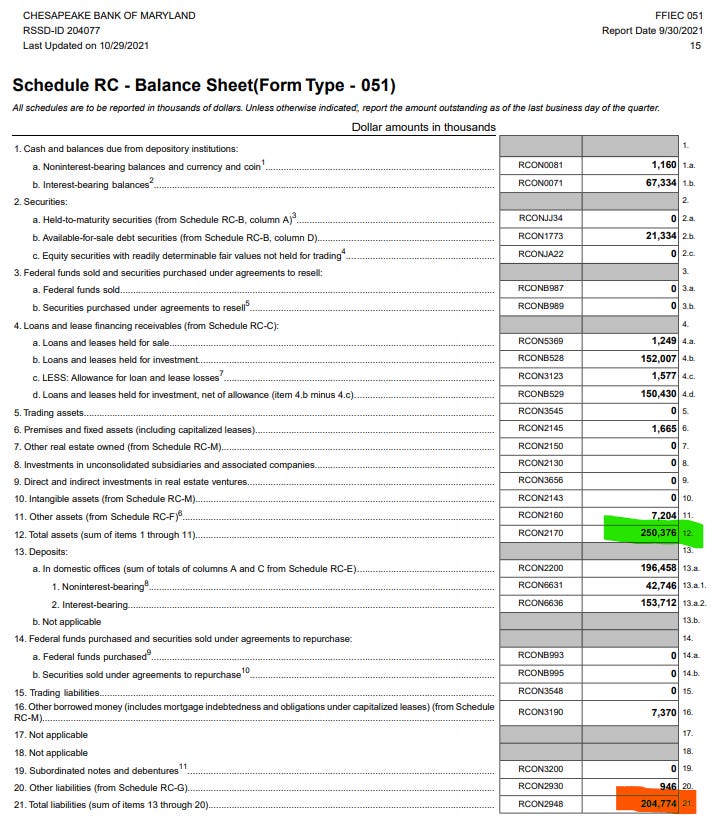

Now one quick note, FDIC call reports and the consolidated financials posted by a company don’t always match up perfectly, but they’re usually pretty close. I am not exactly sure why this is. I suspect bank holding companies may have some level of capital or assets that the subsidiary bank does not. Or perhaps certain liabilities aren’t recognized for regulatory reporting purposes for whatever reason. My hope is that someone in the community can enlighten me! To illustrate, take a look at the 3Q21 CBMB report straight from the company and and 3Q21 call report, the last period when we had both available.

The assets on the balance sheet are pretty spot on but the liabilities are a bit lighter in the company report (above image). The issue seems to stem from a slightly lower level of recognized deposits of $193.6 million vs. $196.5 million. All else equal, lower total liabilities would lead to higher equity levels. Higher equity results in a lower takeout multiple than noted above due to a larger denominator. Since this discrepancy occurred in 3Q21 and a 1.38x multiple seems like a pretty healthy valuation, I’ll assume this quirk remains in 4Q21.

Regardless of the multiple down to the exact decimal point (let’s not get lost in the weeds here), this looks to be a good outcome for shareholders. I’d encourage you to play around with the final multiple and reverse engineer the price you could’ve paid back in 2018 to earn your desired returns.

For example, using a desired 10% return over 3.75 years (assuming the transaction closes June 2022 is approximately 45 months since the conversion), leads to a discount factor of 1.43 (1.10^3.75). Take the final multiple of 1.38x TBV and divide by 1.43. You could have paid ~97% of TBV and achieved your desired outcome, based on multiples alone. Remember, there’s usually some dividends that boost the figure a bit. Ultimately by changing the inputs, I think what you’ll find is “buying right”, or exercising strong price discipline is paramount in thrift conversion investing.

There is one other thing I found interesting and want to note before going. In October 2021, CBMB filed to delist from the Nasdaq and cease SEC reporting, opting to trade on the over-the-counter (OTC) markets. Without being close to the situation, I can only speculate why this was done. Perhaps it was to simply save money (OTC listing fees are lower than the national exchanges), or to repurchase shares from weak hands who didn’t know what they owned and panicked at the price decline associated with the delisting. If the latter, kudos to management in making a savvy play to eliminate additional shares prior to selling the bank.

Okay, that’s it for this week. If you are more familiar than me with CBMB, are a shareholder, and/or know why the two balance sheets are slightly different, please leave a comment below and let me know your thoughts on this transaction. Thanks for reading!

Thank you for your very nice articles. You are probably aware of this already but, if not, here is a good link for looking up the Holding Company reports for banks, which are issued for the 6 months ending June 30 and Dec 31 of each year. This better aligns with what the company will report for its shareholders. As you mention, there are usually more liabilities (debt) and expenses and the holding company compared to the bank, and therefore earnings will be less than expected from the call report alone. https://www.ffiec.gov/NPW

Firstly, are you sure that the dates for each of your set of figures are identical? Just a quarter difference could account for the discrepancy.

Also, since this is a cash deal, there's very little reason to wait 5 or 6 months for your cash if you are a stockholder. The extra 3% that you would get by holding until the closing can likely be dwarfed by investing elsewhere.