First Seacoast Bancorp (FSEA)

Reviewing the prospects of this New Hampshire based thrift with an upcoming second-step conversion

Greetings, and welcome to another issue of Conversion Confidential! I know it’s been awhile, but to my knowledge there hasn’t been much in the conversion pipeline and I only want to write if I have something to say or a bank to evaluate. Today, I’m profiling what appears to be one of the few thrift conversions that will occur in 2023, First Seacoast Bancorp.

Federal Savings Bank was incorporated in 1890 and is based in Dover, NH. In 2019, it changed its name to First Seacoast Bank. Having completed its first-step conversion in July of 2019, efforts are currently underway to execute its second-step conversion. Undertaking a second-step so quickly after the first-step is a refreshing development for investors in contrast to the many thrifts that remain in partially converted limbo for much longer periods of time.

The High Level Stats at 3Q22

Total Assets: $523.8 million

Market Cap: $60.7 million

Dividend Yield: 0%

Loans/Deposits 3yr Growth Rates: 5.4% / 10.6%

9M22 ROA: 0.27% (0.55% in 2021)

3Q22 NPL Ratio: 0.00%

5yr Avg. NCO Rate: 0.00%

PF TCE Ratio: 13.7-15.1% (at min/max of offering range)

PF TBV/Share: $11.85-14.33 (at max/min of offering range)

3Q22 LTD Ratio: 102.4%

Deposits/Branch: $77.3 million

The Transaction

FSEA’s second-step offering has commenced as of November, but will not be finalized for some time. For now, I’ll put up the pro forma tables available in the prospectus. 50% of the proceeds are anticipated to go to First Seacoast Bank, 41.5% will be retained by the holding company, and 8.5% are set aside for the ESOP. Obviously, you’ll want to revisit this once the proceeds from the subscription offering are finalized and apply them to the most recent financials available (which very well may be the 2022 10-K) to capture any changes in equity etc.

The Market

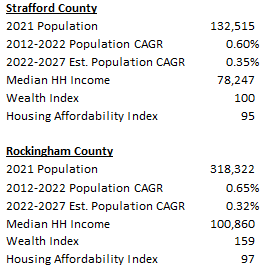

First Seacoast has five branches across southeastern New Hampshire, four in Strafford County and one in Rockingham County. Dover, located in Strafford County is the county seat and the “largest city” (pop. < 50k) in the Seacoast region. In addition, FSEA also considers York County, ME to be within its primary lending market. The greater Seacoast region benefits from growing population and relatively affluent populations.

Per the prospectus, the Seacoast region’s economy is fairly diversified with employment in education, healthcare, government, services, manufacturing and retail. Based on the healthy median incomes, low unemployment rates (2.0% in both counties), and proximity to major metro areas (65 miles to Boston from HQ, as well as under 50 miles from both Manchester, NH & Portland, ME), every indication seems to indicate a relatively healthy local market.

As the table below demonstrates, FSEA has a small but mighty deposit market share in Strafford County which is also growing. This ranks it third behind only TD Bank and Citizens Bank. Meanwhile, in Rockingham, its share is miniscule and shrinking.

Capital

As things currently stand, FSEA sports a 9.1% TCE ratio. Note that this reflects a negative ~$13.5m swing in AOCI from YE21. Also consider that one of the benefits of a first-step conversion is that it allows the bank to manage excess capital a bit more efficiently than a standard conversion. As I state in the high level stats, pro forma TCE ratios are expected to be 13.7-15.1%. This number will move if unrealized losses continue from the AFS securities book or due to net profits in between now and the conversion. While First Seacoast doesn’t exhibit a 20%+ TCE ratio like some of the other thrifts I’ve covered, their capital cushion looks plenty robust to me.

On the regulatory front, things look even better because these capital measures don’t take into account AOCI losses like the standard measure does. As of 3Q22, FSEA has a 15.3% CET1 ratio which is projected to increase to 17.8-18.9% depending on the size of the offering completed. Again, and like most recently converted thrifts, no concerns on the capital front.

Loans Portfolio & Asset Quality

FSEA is a pretty vanilla thrift in that the majority of its loans are 1-4 residential with a decent proportion allocated to CRE ($54.7 million in owner-occupied and $22.7 million non-owner occupied). Most of the underwriting policies look relatively standard for each category. First Seacoast does participate in some purchased loans which is rarely, if ever, smiled upon. At of 2Q22, FSEA had principal balances of $26.5 million in residential purchased loans and $20.6 million in commercial/multi-family participation interests, all of which were all performing. They are all based in the Boston area so they are at least relatively local.

Where I think First Seacoast could struggle is with their asset/liability mix. Over 82% of their total loans are fixed rate (97% of residential) as of June 30th. And with an emphasis in residential and commercial real estate, these are pretty long dated loans. $216 million worth (~56%) won’t mature for more than 15 years and another 22% have maturities in 5-15 years from now. If their cost of funding continues to rise, this will impair spread profitability until they can turn over the portfolio at higher rates. This development will apply to many thrifts and banks out there with long duration assets, not just FSEA.

Asset quality looks great in recent years. As of 3Q22, the balance of NPLs is actually down further to just $5,000, which doesn’t even register as a percentage. Meanwhile, there are no loans categorized as special mention or substandard (down from $3.7 million combined at YE21) and FSEA has no foreclosed assets on the books. Loan loss reserves as a % of loans stand at 0.90%.

I suspect the sound credit quality is a function of a few things: a healthy and mostly affluent market in which FSEA operates, a conservative loan mix focused on 1-4 residential, discipline by management, and a relatively benign economic environment (looking backwards anyway). Given the pristine credit quality, I was curious if First Seacoast held up in the last economic downturn. By using the FDIC’s site, I was able to look further back and indeed, their track record holds up! In the six years including 2008-2013 (some banks are slow to recognize bad loans), NPLs peaked at 1.2% and charge-offs at just 0.28%, both in 2009. First Seacoast was modestly unprofitable that year, but I consider this a pretty strong performance all things considered.

Deposits

In my opinion, First Seacoast has a nice little deposit franchise. As noted above, they own nearly 14% of the deposit share in their home market, gaining a couple percentage points from five years ago. And this isn’t some backwater market with low incomes and/or poor demographics. With 23% of deposits non-interest bearing and core deposits comprising 86% of the total, I suspect an acquirer would find this attractive.

Deposit growth has been respectable at over 10% these past three years, but this may say more about the general environment than FSEA specifically. Watch for that to potentially reverse with liquidity coming out of the system and rates becoming more competitive. You can see a bit of this occurring just since YE21, but to FSEA’s credit, they have also marginally improved the mix by letting time deposits roll of. With a LTD ratio already over 100% however, they have less room to maneuver than some.

On the more negative side of things, I suspect FSEA will always have a hard time efficiently managing operating expenses from a deposits per branch base of only $77 million. Further, FSEA has a large $83 million balance of advances from the FHLB which are 17% of total liabilities. It’s not immediately clear to me why management relies on these so much because an overwhelming majority of these are currently at fixed rates of 2.4-3.15% which obviously doesn’t help their NIMs. Perhaps they were taking advantage of them at lower rates while they could to support loan growth. They appear to be backing off that policy because $20 million of borrowings were retired in advance of their maturities this time last year without incurring any penalties. That may be an acknowledgement it’s not the best practice going forward. Its also worth noting $80 million of FHLB advances mature in 2022/23 so the degree to which FSEA takes out more additional borrowings will be telling.

Management / Corporate Governance

First Seacoast is led by CEO James Brannen, age 60, who joined the bank in 2007 as EVP and CFO. In 2018, he became President and CEO. Brannen has over 30 years experience in New Hampshire community banking and earned an MBA from the University of New Hampshire. Given his age, the conversion combined with a potential future sale of the bank could make sense as an exit for retirement. With total compensation at $458k in 2021, he is pretty well paid for a small bank, but that year is also elevated by a $150k stock award. A $255k salary and $40k bonus doesn’t seem so egregious to me. And yet, relative to his existing holdings, it’s clear his priority will be salary over stockholdings. Brannen does earn a 3x lump cash payment if there is a change in control.

As a group, insiders currently own 1.4% of First Seacoast and this will increase to 2.3% assuming the minimum offering (2.1% at max). I think I’m most disappointed that Brannen is only putting up $50,0000 of his own funds to participate. The maximum allowed in the offering is 40,000 shares, or $400k, and yet only one insider, James Jalbert, gets to even half that amount! For most of the directors, I think this can be excused because my read of the situation is none of them have any direct banking experience. There is the usual with a real estate broker, CPA, and lawyer, but the others appear to be local business owners. However, actual bankers should know better and take advantage of the opportunity.

Per usual, the nine person board is completely “independent” with the exception of CEO Brannen. However, many directors have been in place for a decade or more and one since 1998. One could question whether they will truly view things through an outsider’s lens in order to advocate for shareholders. Directors earn about $67k in total compensation with 2/3rds in stock awards and ~1/3rd in cash. If they serve until age 70, they also earn a supplemental max annual fee of $20k for ten years. Not too shabby. Elections are staggered on three year terms.

In what is hopefully an indication of more things to come, in September 2020, the board authorized and subsequently completed a share repurchase of 5% (excluding shares owned by the MHC). While no dividend policy has been decided on, this shareholder friendly move suggests there is at least some thought given to capital allocation and minority shareholders.

Earnings Power

FSEA won’t win any trophies for driving efficiency gains or impressive returns, but they are consistently profitable. Once again, by going back with FDIC data it appears First Seacoast has generated positive net income every year with the exception of 2009. ROAs seem to hover around 0.30% and prior to the first-step conversion, they used about 10x leverage so ROEs are going to be low-to-mid single digit most likely. As I mentioned, their small stature and low deposits/branch doesn’t suggest much higher profitability is in the cards. You can see this evidenced by an efficiency ratio that jumps anywhere from the mid 70% range to as high as 90%. That said, they are at least saying the right things by emphasizing credit quality, core deposits, and prudently growing commercial lending.

Conclusion

There’s enough to like here for this one to be added to the watchlist in my opinion. The credit quality is strong, a nice little deposit franchise exists, and there is already evidence management will return capital to shareholders. I’ll be keeping an eye on First Seacoast and may arrange a call with management to learn more.

Risks

Profitability - FSEA isn’t very profitable to begin with so returns will be reduced further with additional excess capital. And with a portfolio that skews towards fixed-rate real estate loans, that profitability could be pressured further if interest expenses/funding costs continue their ascension.

Funding Sources - Relatedly, FSEA relies more on FHLB advances than I’d like to see. These are higher cost and hurt margins.

Cyber - In 2018, malware infiltrated the branch office network, but was stopped from accessing customer information by the core processing provider’s firewall. Never a good sign and probably another indicator its hard to balance opex and profitability as a small thrift. The incident cost FSEA $160k and several days of inaccessible data and files.

Time Value of Money - With the second step not occurring until 2023, you likely have to wait awhile for a potential acquisition and prospective IRRs quickly deteriorate depending on how long it takes for value to be recognized whether through a takeover, simple market recognition, or forced appreciation via buybacks.

Corporate Governance - The board of directors largely don’t have banking backgrounds and aren’t very aligned via shareholdings despite a golden opportunity to participate in a thrift conversion. Will they hold management accountable if push comes to shove?

Okay, that’s it for this edition folks. I hope everyone has a very merry Christmas and happy holiday season!

Disclaimer: No position. This is not investment advice nor a recommendation to buy or sell any security. Everything written is for general educational/entertainment purposes and I have not considered your specific financial situation. Always do your own research before making any kind of an investment.

Thanks for the nice write-up and good info. I’m revisiting this as it’s now selling at about 50% of TBV. Any further thoughts?

Thank you for your nice write-up. I have been holding off on buying shares until after the second conversion and after rates stop going up. Their long-dated bonds will keep hurting them further and further until the Fed rate stops going up.