Northeast Community Bancorp (NECB)

A recent second-step conversion with a specialty in niche construction lending

Northeast Community Bancorp (NECB) is headquartered in White Plains, New York and with over $1.1 billion of assets, is larger than many thrifts I’ll profile here at Conversion Confidential. Loans are made predominantly in the NY metro area, including the Mid-Hudson Region as well the Boston metro area in what the bank calls “high absorption, homogenous areas”. NECB recently completed it’s “second step” conversion in July 2021 selling 9.78 million shares at $10/share, for gross offering proceeds of $97.8 million in its subscription offering. The second step comes 15 years after NECB initially went public via it’s “first step” conversion back in July 2006.

The High Level Stats

Total Assets: $1.1 billion

Market Cap: $180 million

Dividend Yield: 2.2%

Loans/Deposits 4yr Growth Rates: 7% / 9%

2020 ROA: 1.31%

3Q21 NPA Ratio: 0.18%

5yr Avg. NCO Rate: 0.095%

3Q21 TCE Ratio: 22.4%

3Q21 TBV/Share: $15.14

3Q21 LTD Ratio: 111%

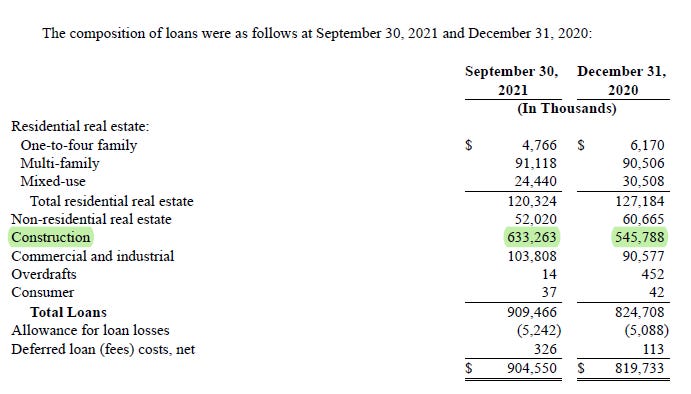

Admittedly, I almost passed immediately when first reviewing NECB. What made me come to this conclusion you ask? Take a look at their loan book…

A whopping 70% of their portfolio is construction loans, up from 40% at YE16! I personally had never seen such a concentration in this type of lending. For the uninitiated, construction loans are probably the riskiest category of loans, given the losses a bank can sustain when economic and/or real estate cycles take a dive. This is a gross generalization, but many banks limit their construction lending to 10-15% (or less) of the loan book. On the flip side, construction loans should be more profitable when done right as they generate higher yields and usually come with a helping of non-interest bearing deposits which improve the bank’s deposit mix and lower funding costs.

I was alarmed by the inherent riskiness, but NECB’s large construction concentration also piqued my interest. What were they thinking, doesn’t management know that kind of concentration is reckless? At the same time I wondered if NECB had carved themselves out some kind of special niche.

Capital

Like most thrift conversions, NECB is over-capitalized so I won’t spend much time here. Personally, this gives me comfort as it increases the NECB’s safety/resiliency. As inherently levered entities, banks get into trouble when they run low on capital to absorb losses from any loans that go bad. Typical tangible common equity (TCE) ratios (TCE/tangible assets) range from 8-12% and anything above 10% is usually considered conservative.

Perhaps the emphasis on construction loans means NECB should hold more capital than another bank, all else equal. 12-15% might be appropriate. However, with a TCE ratio of 22% and a regulatory CET1 ratio of 15.5%, NECB has room for error (margin of safety) in the loan portfolio, as well as capacity for substantial buybacks to “right size” the balance sheet.

Asset Quality

Asset quality has been trending the right direction the past several years with the NPA/NPL ratios declining from 1.6% / 0.85% to 0% in 3Q21 (NECB just wrote off its one $3.6 million NPL at a total loss but with recovery efforts underway - moratoriums are making this difficult as a I understand it). The allowance to total loans looks a bit light to me at 0.58%, but then again, charge-offs are extremely low as highlighted above so management probably knows better than me.

As I’ll detail further in the management discussion section below, NECB operates a very relationship oriented bank when it comes to originating their loans. Borrowers and developers they work with are referred by existing customers. From the 10-K:

The demand for housing (whether for rent or for purchase) is far greater in these high absorption communities than the available supply. This lack of balance between supply and demand leads to available units being under contract of sale or lease assigned very soon after certificates of occupancy are received by the building owners. Generally, in homogeneous communities, units that are under construction have purchase contracts before they are complete.

The underwriting outside of construction loans appears to be conservative. The multi-family loans which are another 15% of the portfolio (when combined with mixed used) have a debt service coverage ratio (DSCR) of 2.8x and an avg. loan-to-value (LTV) ratio of only 36%. Mixed use loans are 2.6x and 30% respectively. Banks and real estate investors alike use DSCRs to assess the coverage of net operating income (NOI) over debt payments. Typically, thresholds range from a minimum of 1.25x to 1.5x on the more conservative end.

So has NECB just been lucky that the economy has done well from the GFC period onward or is there more than meets the eye to this heavily concentrated construction loan book?

Management Discussion Revelations

My conversation with CEO Ken Martinek is where I got truly excited about NECB for the first time. Martinek explained NECB made the decision to move into their construction niche around 2012/2013 after studying the market and realizing a vacuum had been created by two banks leaving the space (acquired by larger organizations who wanted no part of this very specific lending). What is this lending space you ask?

There are two. The most unique is lending to the Hasidic Jewish community, an orthodox community under the guidance of Rabbis who have a tight-knit group of builders NECB is familiar with that construct buildings for their extended families. The other is affordable housing which is essentially all done within the Bronx.

Hasidic Jews tend to have enormous families with 10+ children not uncommon. As Ken explained, this group remembers the horrors of the Holocaust and are determined to never let their numbers come close to extinction again. As such, the population is growing strongly which generates a steady demand. In fact, another reason for conversion was the NY Hasidic communities are growing so fast they were hitting the max loan to one borrower limits. The additional capital raised in the 2nd step increases this limit for NECB.

Here’s where it gets really interesting. Ken stated that no loan has ever been paid late beyond the grace period from this group since 2013. That’s over $3 billion worth of loan originations! The Hasidic community understands that NECB is essentially the only bank left that understands their lifestyle and doesn’t want to risk being cutoff from borrowing. Reportedly, the Hasidic community will also back any individual members who come across hard times and are at risk of default (not unlike other religious groups).

Builders meanwhile, are members of the Hasidic community and have reputational risk if they don’t build quality product. NECB also receives guidance from rabbis and the senior members of the community on which borrowers and builders to avoid, which is valuable information in its own right.

On other topics, I found Ken to be open and forthcoming. I asked him what the “thrift playbook” meant to him. His answer was to use the excess capital to grow with the communities they serve, right-size the balance sheet via the dividend, and potentially pay special dividends. He also mentioned if valuations stay where they are come next summer (after the one-year thrift conversion share repurchase moratorium ends), there would be no reason not to recommend buybacks to the board.

I also pushed him on the board ownership and participation from insiders in the conversion. He answered it was a combo of life situations and that the directors were all intelligent folks, but not necessarily familiar with the opportunity that is a thrift conversion. In my mind, this isn’t the ideal answer or oversight from the board, but I’m just relaying the conversation. Apparently one of the directors is an attorney who closes the majority of deals with the Hasidic community so perhaps there is intangible value that isn’t seen in ownership stakes alone.

Four insiders have bought a combined 7,000 shares on the open market since late August in the low to mid $10 range. This is a pretty weak amount in totality, but is a step in the right direction I suppose.

Management / Corporate Governance

Ken Martinek, 68, is Chairman of the Board and CEO of NECB. He has been with the bank for over 45 years and his grandfather and great uncle founded the bank. Hopefully, this family legacy means there a degree of higher stewardship and better oversight as a result. After all, a bank’s first and foremost priority is maintaining credit quality and not risking a blowup.

NECB has a classified board where directors are elected to three year terms. None of the insiders own a material amount of stock despite long tenures on the board and none participated to the maximum amount allowed in the offering. The closest was CEO Ken Martinek who subscribed to 20k shares (the max was 30k). The average age of the nine person board of directors is 65 years which could mean a willingness to sell down the road, but the family aspect of it may make that less likely.

Material weakness in internal controls. NECB made improper postings of loan origination fees and costs in 2019 and 2020, leading to $864 thousand and $1.2 million of recorded interest income to be reversed. The corrections also simultaneously reduced non-interest expense and had no impact on net income of the bank. Not the biggest deal in the world, but not ideal either.

Famed thrift enthusiast and small bank activist Joe Stilwell of Stilwell Value owns ~4.3% of NECB. Interestingly enough, Stilwell Value has a written agreement to support the board’s nominees and proposals (essentially no activism) for five years as part of the deal to finally fully convert. Stilwell Value recently held over 8% of shares outstanding, but has been selling down the position. My understanding (based on a conversation with Joe) is that the holding no longer qualifies for his activist fund given the shareholder agreement.

Deposits

NECB doesn’t have any major deposit market share in any of the counties it does business (highest is 0.67% share in Rockland County). Additionally, core deposits as a % of total deposits are only 62% as the bank relies more on brokered deposits than I’d prefer. NECB has over $200 million in CDs rolling off in the coming year, but replacing them is lower priority given their low current cost. NECB has a direct relationship with the military as a source of their deposits. They match the duration of these sourced military deposits with construction project durations.

As a result of its close commercial/builder relationships, 38% of NECB’s deposits are non-interest bearing! This is an impressive ratio and helps explain the profitability of the bank.

NECB also remains committed to opening branches within the Hasidic community. I don’t love this as I’m not sure the role/necessity of bank branches in the future, but I did find an article from 2016 that stated a then newly opened branch brought in $45 million in deposits in only four months. It’s harder to argue with that kind of traction!

Earnings Power

Typically, I don’t spend much time on a thrift’s earnings power, or lack thereof. NECB is different in this regard and it’s worth highlighting. Two things jump out, uncommonly strong ROAs as well as a decent efficiency ratio. As discussed, NECB generates higher profitability from their specialization in unique lending areas. This and the fact NECB is larger than many thrifts probably helps the efficiency ratio (a measure of opex to total income - lower is better) register a reasonable figure because they can spread fixed costs a bit more effectively. It is not uncommon to see many small banks operating with 75%+ efficiency ratios which is horrendous.

So What’s it Worth?

Banks are valued on a number of different measures which I’ll highlight in later posts. Recently converted thrifts tend to be small, subscale, and overcapitalized. This often leads to unacceptably low ROEs, partially from their traditionally low yields and high cost structure, and partially from the impact of low leverage (remember low leverage makes them less risky though). As a result, I believe think thrift valuation should be assessed on multiples of tangible book value and core deposit premiums.

Briefly, core deposit premiums represent the price premium as a percentage of core deposits an acquirer pays over tangible equity in the acquired bank. Historically, this figure tended to range from 5-15%, but should probably be closer to the lower end with interest rates as low as they are. It’s easier now than ever for banks to access low-cost funding sources, but this may not be a permanent fixture.

As of 3Q21, I have NECB down for $496 million in core deposits. Applying a 5-10% core deposit premium results in a per share value of $16.67-$18.17. Meanwhile, at 1.25x TBV, NECB is worth ~$19, today. This is before adding the bank’s earnings over the next several years or any impact from accretive share repurchases (done at discount to TBV) and/or dividends. Remember, NECB pays a 2.2% yield currently.

Notably, NECB generates respectable ROEs (high single-digits) despite having 15% equity ratios. ROE figures will obviously come down due to the additional capital in the conversion, but if NECB can maintain the 1.2% ROA they averaged the past five years, one could reasonably expect another $13 million of net income added to the bank’s equity per year (before dividend payout).

In the below table, I’ve laid out a simple range of IRRs one might be able to reasonably expect by buying near the current price of $11 per share (73% of TBV) and assuming it reaches the low/high end price targets based on my core deposit premium and TBV multiple valuations. Should NECB trade at a premium to TBV? I would say so even if they aren’t a takeout target based on the profitability of their lending. Pay attention to the returns at the 3/yr mark, as this is the first year regulators will allow a thrift to be sold. This tends to be when investors bid up thrifts to at least book value and sometimes beyond.

My best guess is you can expect 10%-15% returns plus dividends. These aren’t the sexiest, life-changing returns, but thrift conversions have a formula that tends to work without taking on excessive risk. Considering where valuations are for many areas of the market, this strikes me as a pretty reasonable bet for the next few years.

For those who may not be familiar, there are two catalysts that play a prominent role in helping close the gap between market prices and intrinsic value in thrift conversions. The first is share repurchases. Management is allowed to buyback shares after the one year anniversary of a conversion. Ideally, these repurchases are done at discount to book value which is an accretive and intelligent use of capital. The second factor is M&A activity. The U.S. is over banked and a wave of consolidation has been occurring the past few decades. Subscale and overcapitalized thrifts are a target for acquirers who want access to a low cost deposit base, cut overhead expenses, and leverage the asset base to earn double digit returns on equity.

Risks

Credit losses - since NECB only moved into their construction niche in 2013, we haven’t seen the potential impact from a negative economic environment. NECB was not spared from losses going back to the GFC although they were quite manageable. Still, so much construction lending makes me a bit uneasy so know the risk you’re taking and size your position accordingly.

Capital allocation - there’s always a risk that a board with low ownership supports dubious corporate actions or refuses to sell the bank in order to continue collecting their director’s fees. However, if NECB is going to earn low double-digit ROEs or more, there will be less pressure on them to sell.

Liquidity - the LTD ratio of 111% and reliance on brokered deposits is a bit more aggressive than I’d prefer.

Disclaimer: I and others I advise are long NECB shares. This is not investment advice nor a recommendation to buy the security. Everything written is for general educational purposes and I have not considered your specific financial situation.