TC Bancshares Inc (TCBC)

A small thrift on the Florida-Georgia line to keep your eye on

Welcome to another edition of Conversion Confidential and apologies for the late publication. I’ve been a bit preoccupied recently (I’m happy to report my real estate license was successfully renewed at the 11th hour), so I think it’s about time to profile another thrift, and one that I believe is worthy of inclusion on your investment radar.

TC Federal Bank was organized in 1934 and chartered in 1937 as a mutual savings and loan association. Last July, TC Federal undertook a standard thrift conversion, selling 4.9 million shares at an offering price of $10 per share, raising gross proceeds of $48.9 million in the process. Net proceeds of $47.7 million were split as follows:

$23.9 million contributed to the bank,

$3.9 million used to fund the loan to the employee stock ownership plan, and

$19.9 million retained by the company

Shares of the newly created TC Bancshares common stock began trading on July 21, 2021 and closed at $12.11 per share.

The High Level Stats (1Q22)

Total Assets: $397.9 million

Market Cap: $66.4 million

Dividend Yield: 0%

Loans/Deposits 3yr Growth Rates: 4.8% / 8.8%

1Q22 Annualized ROA: 0.70% (2021: 0.72%, 2020: 0.18%)

1Q22 NPL Ratio: 0.11%

5yr Avg. NCO Rate: -0.076%

1Q22 TCE Ratio: 21.7%

1Q22 TBV/Share: $17.59

1Q22 LTD Ratio: 89.2%

Deposits/Branch: $153.4 million ($76.7 million if you count two loan production offices)

The Market

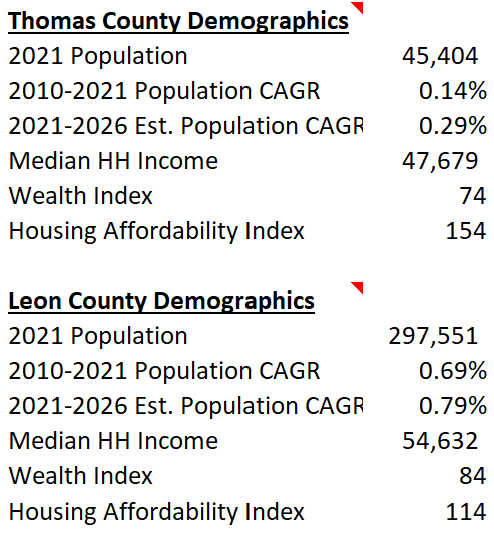

TCBC is headquartered in Thomasville, Georgia which is approximately 35 miles north of Tallahassee, FL. It’s primary markets consist of serving retail and small businesses in Thomas and Chatham counties in Georgia as well as Leon County in Florida.

Thomasville is the county seat of Thomas County and plays host to the annual Rose Festival. Despite its small size, (county population estimate is only ~50,000), Thomasville is also home to another public company, Flower Foods (NYSE: FLO), the second largest baking company in the nation. The largest regional employers are Archbold Medical Center and Thomas County School System.

Given the small nature of its home market, it’s no surprise TCBC has also sought to expand into neighboring city Tallahassee, FL as well as Savannah, GA. Tallahassee, located in Leon County is the capital of Florida, the county seat, and home to Florida State University (FSU). It’s also the fastest growing economy per capita in Florida. Leon County’s estimated population as of 2021 was ~300,000 and the largest employers are the State of Florida, FSU, and Tallahassee Memorial Healthcare.

Savannah is the oldest city in the state of Georgia and is the county seat of Chatham County. In 2021, Chatham County had an estimated total population of ~290,000. The largest employers in Chatham County are Gulfstream Aerospace Corporation, Memorial Health University Medical Center and Savannah-Chatham County Board Education. Interestingly enough, Savannah is also home to the largest single-terminal container facility of its kind in North America. The Savannah market looks just fine to me, but given the distance and lack of a current foothold, I’m a bit less optimistic about expansion into the area.

Finally, TCBC announced its expansion into Jacksonville, FL in April. They noted many community banks in the area have been acquired by larger institutions. Leading the Jacksonville team as market president will be long-time local banker Jeff Weeks. Weeks has led commercial lending teams for over two decades and has over 30 years of total experience. TCBC intends to begin with a commercial loan production office followed soon after with a retail branch in the market.

Capital

Fresh off a standard conversion, TCBC is significantly overcapitalized with a TCE ratio of 21.7%. Like many small thrifts, their biggest challenge will likely be deploying all that excess capital in a prudent and timely fashion in markets with more competition. On the regulatory front, the CET1 ratio of 24.6% is even stronger. No concerns here.

Loan Portfolio / Asset Quality

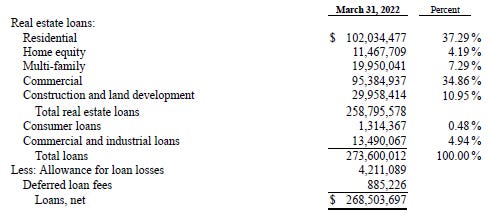

TCBC has a pretty traditional loan book with a historical emphasis in residential and commercial real estate (CRE). TCBC also had notable participation in the PPP program which drove 2020 loans by an additional $25 million and temporarily skewed the ratio of commercial and industrial (C&I) loans. Going forward, they intend to diversify the portfolio away from residential real estate by focusing originations on CRE, multi-family, C&I, and construction loans. By comparing the current loan mix to that noted in the S-1, we can see the effects of this transition already underway. Residential real estate has come down somewhat from the 45% of loans in 2016. Similarly, back in 2016, C&I loans represented less than 2% of the total. Today, it’s more like 5%. About 61% of the book is floating, or adjustable rate loans.

Looking back over the past couple years, the credit quality shows a bit of a mixed bag. NPL/NPAs are more elevated than I’d like to see, particularly in what has been a favorable economic backdrop, although 2020 was an exception. Asset quality continued to improve in 2021 with the NPL and NPA ratio at 0.15% and 0.40% respectively. The NPA ratio is also much lower (0.14%) when adjusting for the fact that $1 million worth of real estate owned is actually guaranteed by the SBA. Meanwhile, TCBC’s reserve for loan losses looks good both as a percentage of loans and relative to non-performing loans.

I suspect the main reason credit quality has struggled somewhat is the relatively low median income in the main market. Many real estate investors I know want to see median household incomes of at least $45,000 for an area, so at just over $47,000, Thomas County is barely exceeding this threshold. I would expect this demographic to get hit disproportionately by an economic downturn so perhaps the loan book is a bit more vulnerable.

What’s interesting however, is that the higher NPL ratios rarely result in meaningful charge-offs. In three of the past six years, recoveries have exceeded charge-offs, which included 2021 (not pictured above). This could be an indication management is conservative in their loan evaluation which is a positive.

Classified and criticized loans have been creeping up, predominantly led by special mention loans. In 2019, they were $6.8 million rising to $15.9 million in 2020 and $17.1 million in 2021. At 1Q22, they had declined back down to $12.1 million as commercial special mention loans improved.

Deposits

I have to say I am largely impressed with the deposit franchise at TCBC given its small stature. As noted above, TCBC owns 14% of the deposit share in their home market, although this was down a couple percentage points from five years prior. Core deposits represent about 75% of deposits, again pretty good for a small community bank. They have also been growing faster than CDs as the core deposit mix improved from 60% in 2019. As of 1Q22, 13.1% of total deposits are also non-interest bearing, up from 5.6% in 2019. The real test may be still yet to come however as these deposits will need to prove themselves sticky in the newly arrived rising rate cycle.

Management / Corporate Governance

I believe corporate governance may be the Achilles heel of TCBC. That’s not to say it’s the most egregious I’ve ever seen, but the setup isn’t exactly promising either. To start, TCBC’s board of directors consists of seven members who are elected to three year staggered terms. Nothing new there. There had been an eighth director who was a local veterinarian, but he was rightfully retired in connection with the conversion. Director fees range from $32,000 - $42,000 (with the exception of Mr. Brown) and are paid in all cash.

G. Matthew Brown retired at the end of 2020, having served in CEO role since July 2018 after only having joined the bank in March 2017. He now serves as a consultant to TCBC to the tune of $75,000 per year, in addition to his director fees. For some reason, that bugs the shit out of me. Sure, he has a lot of “experience” having been a banker his whole career, but is it worth paying for? The results don’t show it in my opinion. Perhaps it’s just that I’ve seen a lot of these shenanigans in thrift land or the fact that he was at the helm (as was CFO Linda Palmer) of Premier Bank which went bankrupt back in 2012 under his leadership. This feels like a cush way to pull in a little salary in addition to director fees for what is probably incredibly undemanding work. Is it also a coincidence he owns fewer shares than all other directors except one? I doubt it!

TCBC is now led by Greg Eiford who took over starting in 2021. Eiford has been employed with TC Federal since 2008 in roles such as Senior Lending Officer and Executive Vice President. Prior to that he owned a residential home builder and a Christian Book Store, both up until 2008.

I’ve had the opportunity to speak with CEO Greg Eiford twice now. I liked him and thought his answers to my questions were reasonable enough. He explained he’s conservative in classifying trouble loans which seems to check out based on my above analysis. He also owned up to the mistakes the bank made in the past, such as underwriting non-owner occupied residences as primaries rather than income producing CRE requiring certain interest coverage thresholds. There is a new senior credit officer and three new underwriters in place since the time when the bank was making losses. Eiden also seemed quite interested in the “thrift conversion playbook” when I shared with him how FFBW Inc. is engaging in significant share repurchases. He also recommended I read The Outsiders which most investors are already familiar with. In theory, that’s a good sign!

What concerns me as an investor in this thrift conversion is his age. Eiford is only 51 and is poised to make over $350,000 per year in total compensation. TCBC will be eligible to be acquired in just over two years. But you tell me, if you’re 51 and pulling in $350k+ in a lower cost part of the country, what incentive do you have to sell the bank? The change in control provision in his employment agreement only calls for 2x the sum of his salary and the average bonus paid out to him over the previous three years. Add in the fact that Eiden has no material stock ownership and the answer is he probably won’t sell, not for awhile anyway. I don’t think I would either. The problem this presents the investor is the associated opportunity cost. It’s probably fair to assume the valuation ceiling on a small bank like TCBC is 1.4x TBV and that may be overly generous. If it’s going to take a decade to realize that valuation, you’ve seriously limited your potential IRRs even if buying at a compelling entry price.

Named executive officers are incentivized on several financial metrics including net income, deposits (volume and accounts), and the bank’s efficiency ratio, as well as more subjective components. Exact targets however are not disclosed. It’s also worth noting that in May 2021, Noel Ellis, who served as EVP and Chief Credit Officer resigned for “personal reasons”.

The maximum purchase amount in the subscription offering last July was $300,000 for an individual and $400,000 if combined with a spouse. Unfortunately, none of the directors or executives fully subscribed. In fact, only two directors came reasonably close putting in $200,000 of their own capital. I view this as pretty disappointing, but it also isn’t all that uncommon. Insiders in total acquired 106,500 shares which represents ~2.2% of the shares now outstanding. Now that we have the benefit of a proxy statement, we can confirm insider ownership remains at 2.3%. I’d like to see insiders start purchasing shares on the open market in significant sums given the current valuation. Only time will tell if they’ll step up to the plate, but if management doesn’t believe in the opportunity, why should minority investors?

As of March 28th, there were no shareholders of note owning 5% or more of the bank. Given the potential here, I would surprised if this doesn’t change over the coming year or two. I think TCBC would do well with the influence of an activist. What’s more, I think some of better known bank activists would have interest in the TCBC given the potential here.

Earnings Power

I liked the focus and verbiage from the S-1 on TCBC’s current business strategy. Point number one was to improve the operating efficiency of the bank, which implemented a new core processing system in 2020. Truthfully, they’ve got some work to do here as the below table indicates, but core processing transitions can be painful and this led to increased costs in 2020. They have also stated operating expenses will increase as a public company so they’ve got their work cut out for them in this area. Despite this, the efficiency ratio dropped to 76.7% in 2021 which remains unacceptably high but at least trending in the right direction.

Other priorities included increasing core deposits, growing the loan portfolio prudently, and maintaining credit standards…all the standard verbiage you want to see. To their credit, they have been profitable each of the last six years despite an elevated expense base.

I do think like most residentially focused banks, TCBC will miss the surge in gains on sale of mortgage loans from the past two years. This probably represents a headwind of $1.5 million to $2 million. However, if TCBC can eek out a normalized ROA of 30-50bps, they can probably add anywhere from $1.2 million to $2 million in net income on average each year. I know that’s not exactly a high bar, but TCBC is also not above net losses either. While net income has been positive from 2016 on, it was negative for six consecutive years from 2010 through 2015 according to the FDIC. This is a bit of a cause for concern.

Valuation

TCBC reminds me a bit of FFBW Inc, which I have written about a number of times, most recently here. The bank is obviously small and subscale, yet located in a decent enough market with seemingly the right priorities in maintaining asset quality and plans to return capital to shareholders. Of course, being earlier in their journey, TCBC still has plenty to prove when it comes to returning capital. I’m looking forward to the potential announcement next month. I believe management and the board can make an immediate statement by initiating with a 10% repurchase authorization as opposed to the traditional 5% buyback.

At 76% of TBV currently, TCBC’s valuation certainly isn’t demanding. The question is what might it be worth today, what could it be worth a few years from now, and what is the probability it reaches those estimates. For starters, I’ll throw out a core deposit premium range of 5-10% reflecting increasing interest rates and a pretty respectable deposit profile at the bank. That means the TCBC could be worth approximately $20-$22.40 to an acquirer today. Alternatively, if they earn $1.5 million or so for the next several years and repurchase 10% of shares outstanding each year, a TBV multiple of 1.2x should also get them to $22+ per share. On the low end, I think they should be worth at least 1x TBV unless losses begin to pile up again. So let’s call fair value anywhere from $17.60 on the low end to $23 per share on the upper end. Below is a simple table of returns you might expect if any of those price targets are reached within the corresponding timeframes.

As I alluded to, I can foresee this one being drawn out which will eat into an investor’s returns. If this takes over five years to realize value, the potential IRRs will become far less intriguing pretty quickly. As I mentioned, watch for the repurchase announcement next month which will give a better indication how serious management is about rewarding shareholders. Additionally, I think TCBC will get much more interesting if a respected activist comes aboard.

Risks

Asset quality - How resilient will TCBC be in a tougher economic environment? The home market is relatively low income and the bank has experienced extended periods of net losses in the past.

Time value of money - Management at TCBC is relatively young and hasn’t been at the helm for very long. It would not surprise me if the bank is still public five years from now.

Corporate governance - Aside from the usual thrift misalignment, insiders also don’t own much of the stock while having little reason to sell the bank anytime soon, which gets at the point above.

Okay, that’s all for this issue folks. Thanks for reading and if you like what you’re seeing then please don’t hesitate to share with your friends!

Disclaimer: I and others I advise are long TCBC shares. This is not investment advice nor a recommendation to buy or sell any security. Everything written is for general educational/entertainment purposes and I have not considered your specific financial situation. Always do your own research before making any kind of an investment.

Good enjoyable writeup.

Looks to me like a situation to watch rather than to own.