Using Regulatory Reports

Regulatory reports filed with the Federal Financial Institutions Examination Council (FFIEC) can aid bank investors

Greetings and Happy Easter! The family is coming over shortly so today’s issue will be a bit shorter. I’m optimistic it will still add value to those of you who are unfamiliar with these reports. So for starters, have you ever wondered how a bank might have performed in the most recent reporting period, but had to wait several months until the SEC reports were finally filed to let you know? If yes, then you’re in luck.

As a heavily regulated industry, all financial institutions in the U.S. are required to file periodic financial reports with regulators. This is in addition to SEC filing requirements. Basically, if you are a bank insured by the Federal Deposit Insurance Corporation (FDIC) then you are required to file a quarterly report with the Federal Financial Institutions Examination Council (FFIEC). Who is the FFIEC you ask…

The Council is a formal interagency body empowered to prescribe uniform principles, standards, and report forms for the federal examination of financial institutions by the Board of Governors of the Federal Reserve System (FRB), the Federal Deposit Insurance Corporation (FDIC), the National Credit Union Administration (NCUA), the Office of the Comptroller of the Currency (OCC), and the Consumer Financial Protection Bureau (CFPB) and to make recommendations to promote uniformity in the supervision of financial institutions.

The Council is responsible for developing uniform reporting systems for federally supervised financial institutions, their holding companies, and the nonfinancial institution subsidiaries of those institutions and holding companies.

The reports required by the FFIEC are formally known as the Consolidated Report of Condition and Income, or more generally referred to as a call report. Banks file call report forms FFIEC 031, 041, or 051 depending on the bank’s size and whether or not it has foreign operations.

One fun fact according to Wikipedia is that thrifts used to file a related report known as the Thrift Financial Report (TFR). Following the merger of the Office of Thrift Supervision (OTS) and the Office of the Comptroller of the Currency (OCC) however, thrifts had the option of filing either a call report or a TFR. Beginning with the first quarter filing in 2012, all thrifts were then required to file a call report and no longer able to file a TFR.

For investors, call reports can be found at this link. Just search for the bank you’re interested in and you can pull up a PDF of its operating results. A quick word of warning. The site’s search function is not quite up to Google’s standards. If you don’t have the name of the bank just right, it may not turn up anything in the search results. Also keep in mind that the call report is filed at the operating bank subsidiary level, not necessarily that of the incorporated bank holding company which trades publicly.

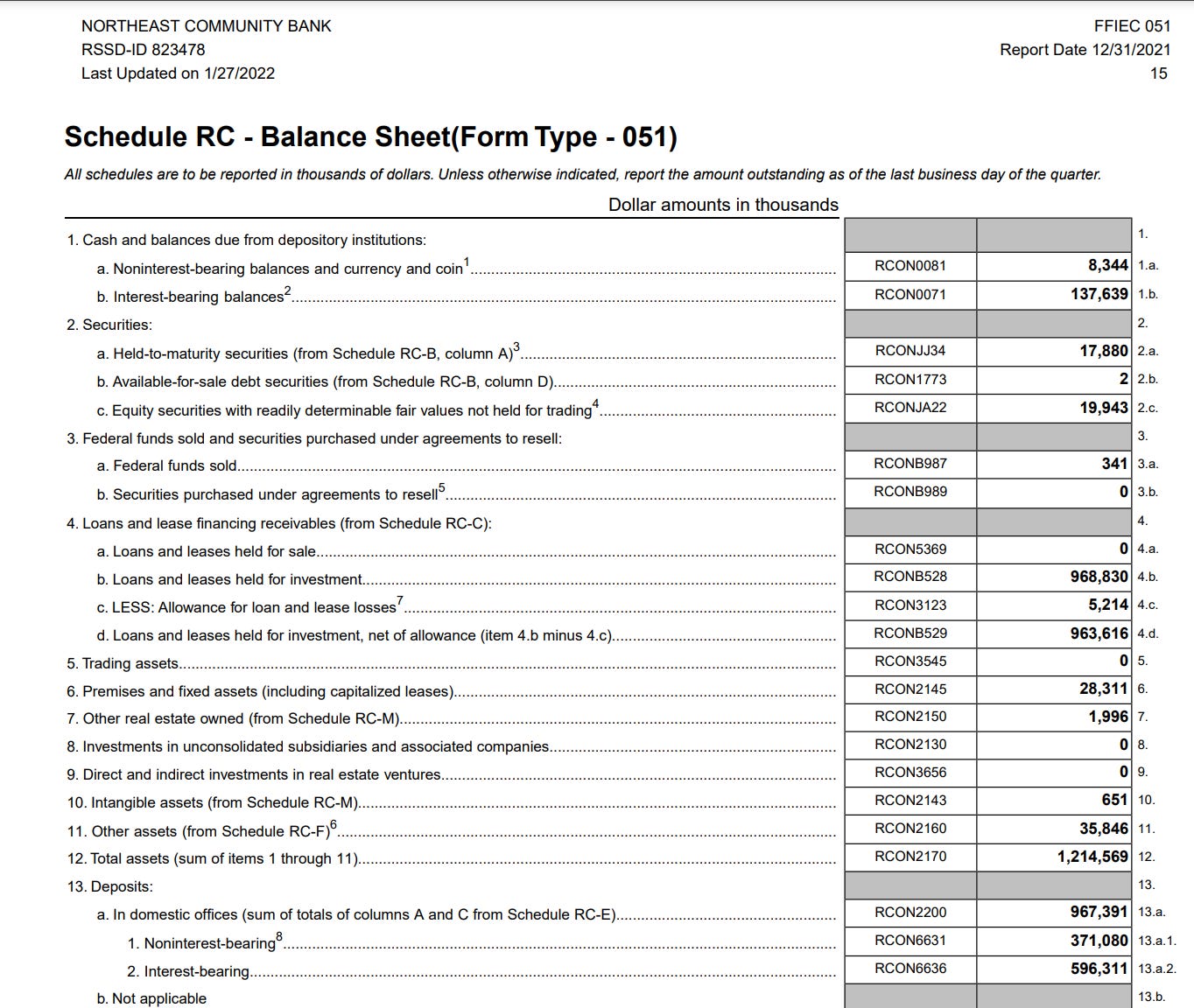

I have included a snapshot of part of the balance sheet for Northeast Community Bancorp as an example. You’ll notice that the call report is thorough and has a full balance sheet, income statement, data on loan losses, deposits and more. Just about anything a federal auditor might want to know to evaluate whether the bank is getting itself into trouble is included.

So why is this helpful? Well, call reports are required to be submitted no later than 30 days past the end of the fiscal quarter. For example, 1Q22 reports will be due by the end of April. The publishing of a call report may or may not line up with SEC disclosures. In instances where the call report comes out before SEC reports, it provides savvy investors a first look at the bank’s results. Often times, banks will time it so there is at least a press release that comes out simultaneously with the call report, but not always. And for “non-reporting” banks, a call report might be your only insight into performance if management isn’t treating their bank as public entity.

Now I mentioned above that the call report is for the subsidiary bank. This means it may omit some important information. Cash is often also held at the parent holding company level, particularly in the case of thrifts when they convert. Cash proceeds from the offering are often placed at both the parent holding company and subsidiary bank (the prospectus will say exactly how much goes to each). Fortunately, the FFIEC has a separate site where you can pull this data parent holding company data as well. It is formally known as FR Y-9SP report. Thanks to reader VA Investor for sharing the link with me several months ago when I wrote up the CBM Bancorp acquisition!

Here again, I’ve included an image of the subject report depicting NECB at 4Q21. You can see the equity investment the parent company has, which is simply the subsidiary bank and that there is cash at the parent level as well.

Okay so there you have it. Between those two regulatory reports, you should be able to piece together a pretty accurate portrayal of the bank’s financial standing and operating results, with or without the help of formal SEC filings. That’s all for this week folks, thanks for reading and Happy Easter!